Two methodologies.

One workspace.

Salary on IRC §162 + BLS. Basis on §1366/§1367 + Form 7203. Both transparent, repeatable, audit-ready.

Reasonable comp

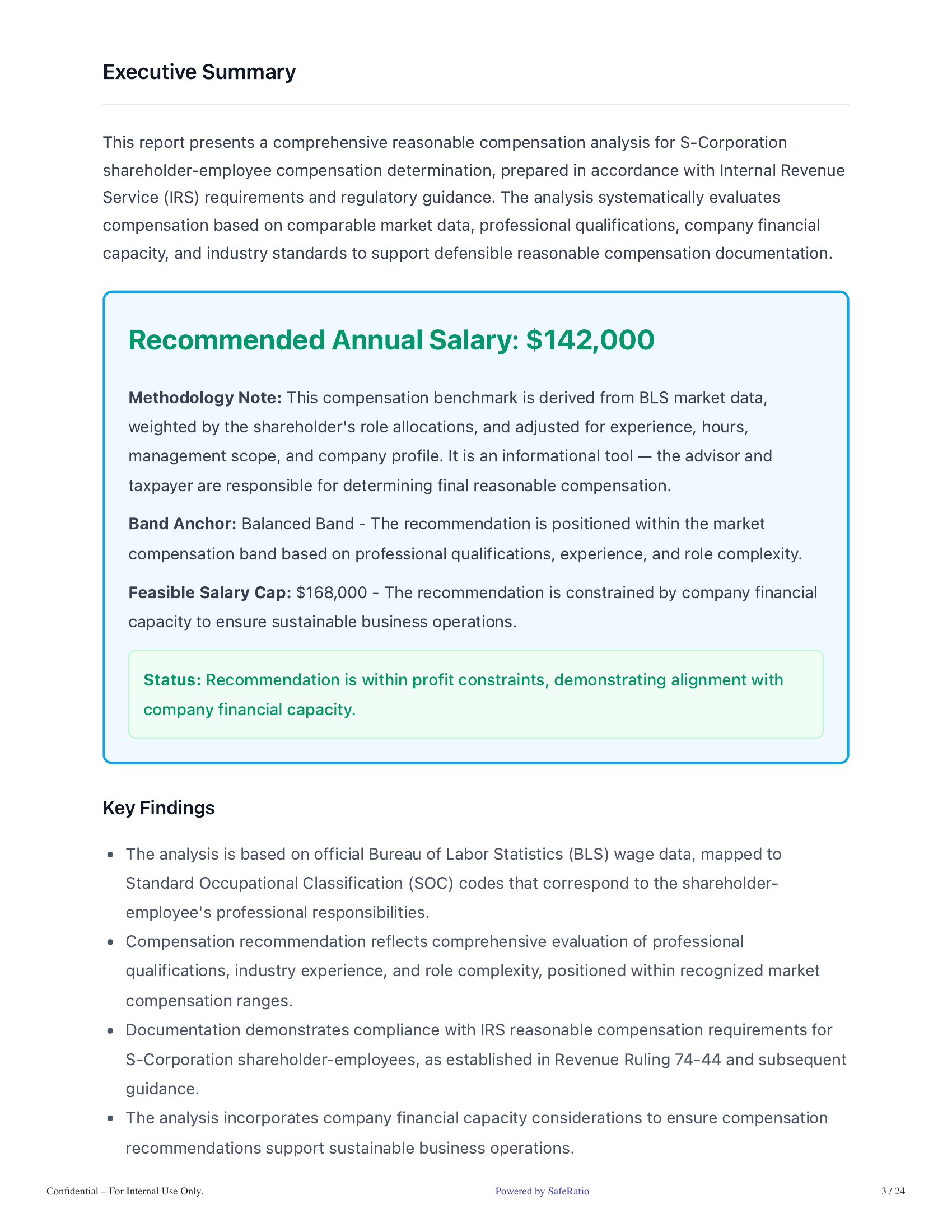

Three IRS-recognized approaches on a 6-step pipeline. BLS OEWS wage data. Confidence-scored.

Shareholder basis

§1366/§1367-ordered stock-basis cascade. Form 7203 import seeds prior-year history. Year-over-year correct.

A six-step analysis pipeline.

Six inputs run through one pipeline. The output: a salary range, a confidence score, a methodology trail, and the audit-ready report.

Role & duties

What hats?

Financials

Revenue · scale

Market data

BLS OEWS

Defensibility

Cross-validate

Confidence

0–100 score

Report

PDF · audit pack

Three IRS-recognized approaches

Cost, income, and market approaches.

Three perspectives on the same shareholder. When the approaches agree, the result is highly defensible. When they diverge, the report flags it for further review.

Cost approach

Many Hats Method

What would it cost to replace every role the shareholder performs?

Marcus Reyes · weighted roles

Income approach

Independent Investor Test

Does the company still earn a reasonable return after paying the proposed salary?

Atlas Mfg · post-salary return

Market approach

Industry comparison

Direct salary benchmarks from comparable companies in the same industry + region.

Distribution · 248 comparable firms

Blended → Recommended

$118,400

Weighted average of all three approaches. Defensible range: $85K–$144K.

Confidence

87%

All 3 approaches agree

The §1367 cascade,

in statutory order.

Stock basis arithmetic is non-commutative. A common source of basis errors is applying these steps in the wrong sequence; SafeRatio applies them in the order §1367 prescribes.

Reconciles to $0.00

Cascade arithmetic

Marcus Reyes · TY 2026 · §1367(a) ordering

Why the order matters

Distributions are subtracted before losses (§1367(a)(2)(A)). Reverse them and you'll deduct losses that should be suspended — and the distribution might land tax-free when it should produce gain.

Form 7203 onboarding

Form 7203 mapped

to the ledger.

Each Form 7203 line corresponds to a ledger entry. Sub-totals are validated against the form's identities before any entries are written.

Identity checked

L5 = L1+L2+L4

✓ closes

Parser confidence

~1.4s · OCR-free

✓ math validates

Rolls forward

L15 → next opening

✓ no manual re-entry

Why both pillars together

One salary number, used three ways.

Salary analysis output

$118K

Recommended salary from the three-approach analysis.

Forecast officer comp

+$118K

Flows in automatically as officer compensation on the P&L grid.

Resulting ending basis

$26.3K

After the K-1 share is allocated and distributions are drawn down.

The deliverable

Every methodology step cited.

24 pages. Inputs, BLS data sources, calculation steps, IRC §162 references, and the defensibility rationale. Attached to the file as the report generates.

Download the 24-page sampleMethodology trail

Inputs · sources · logic

Every step of the methodology

cited in the report.

Salary on IRC §162 + BLS OEWS. Basis on §1366/§1367 + Form 7203. Inputs, sources, and logic all in the file.

Exhibitor at NAEA Tax Summit 2026